The importance of developing the accounting information system to enhance the efficiency of value chain analysis of Iraqi economic units

Keywords:

Develop the information system, enhance the efficiency of value chain analysisAbstract

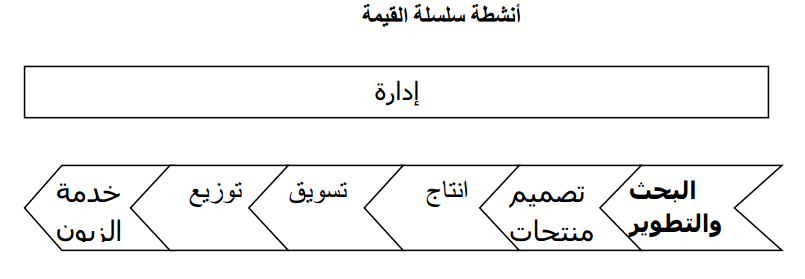

The paper aims at shedding light on some important aspects that entail the development of Accounting Information System to apply an alternative model of strategic dimensions. This model is exemplified by the value chain. The paper also aims at introducing some methodological steps to analyse the activities of this chain and show the best way to make use of it in dividing the activities into value added activities and non-value added activities, taking into consideration the importance of relying on measuring the efficiency Time of Value Chain Activities.

The paper is based on a hypothesis which claims that Business Environment impels any Economic Entity to adapt to the variables of this environment to keep pace with the technical development and competition. This requires the development of the information systems of this entity, the most important of which is the Accounting Information System. This development must parallel the development in the methodologies and tools of administration such as Value Chain Analysis to enhance the efficiency of the administration analyses.

The applied case is based on the analysis of some of the activities of the Value Chain in The Electronic Industrial Company in Iraq. The paper reached at a number of conclusions, the most important of which are (1) the use of the value chain analysis helps the economic entity in managing their costs by means of analyzing its activities and dividing them into primary and supporting activities besides defining the periods which such activities require. This contributes to the analysis of the value which such activities add to the product. (2) The economic entity, the sample of the paper (i.e., the Electronic Industries Company) uses classical concepts of accounting which is of limited efficiency that is unable to face the dramatic changes, especially in the field of manufacturing the electronic products and its related services which depend on innovation. (3) The company suffers from a decrease in the efficiency of the time of activities which add value as opposed to an increase in the time of activities which do not add value. This conclusion is based on a general, descriptive, and quantitative analysis of the value chain of one type of electronic products (television) by means of analyzing the efficiency of the times of the production activities (assembly and finishing) during the manufacturing processes and the related activities which add value to the product.

References

. Foster, George, Mahendra Gupta, and Leif Sjoblom, (2001), “Customer

Profitability Analysis: Challenges and New Directions”, Readings in

Management Accounting, Prentice-Hall

Hergert, Michael, and Deigan Morris, (1989), “Accounting Data for Value

Chain Analysis”, Strategic Management Journal, Vol. 10, No. 2 (Mar. – Apr.),

pp. 175-188.

Horngren, Charles T., Srikant M. Datar, and Madhav Rajan, (2012), Cost

Accounting-A Managerial Emphasis, Prentice Hall. P. 6.

Kaplan R. S., (1984), “The evolution of management accounting”, The

Accounting Review, Vol.59, No.3, pp.690-718.

Kinney, Michael R., and Raiborn Cecily A., (2011), Cost Accounting-

Foundations and Evolutions, South-Western Publishing.

Lanen, William N., Shannon W. Anderson, and Michael W. Maher, (2011),

Fundamentals of Cost Accounting, McGraw-Hill Irwin.

Porter M., Competitive Advantage, (1985), Free Press Inc.

Shank, John K. and Vijay Govindarajan, (2001), “Strategic Cost Management

and the Value Chain”, Readings in Management Accounting, Prentice-Hall.

and the Value Chain”, Readings in Management Accounting, Prentice-Hall.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2014 Economics and Administration College - Karbala University

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.