Financial crisis and its implications in the policy of dividends (Case Study)

DOI:

https://doi.org/10.71207/ijas.v8i31.3120Keywords:

Financial crisis, policy of dividendsAbstract

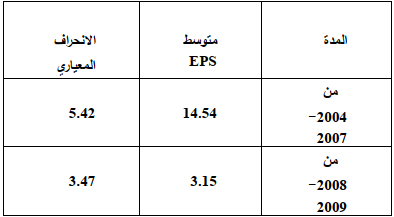

The purpose of this study is to search in the international financial crisis and its reflections in the dividends policies for a sample of listed companies in Dubai Financial Market.

The study launched from the cognitive dimensions for the two concepts of the financial crisis and the dividends policies to show the dependence or the change of the followed policies of dividend of the companies before the occurrence of the financial crisis which stormed the international financial markets and shifted to the other markets such as the evolving markets and to the markets of Arab Gulf countries, especially Dubai Financial Market, because of the importance of dividend policies, since they are the most important financial decisions as a source of internal financing for the firms and return on investment of the shareholders from one side, and their reflections on the prices of the shares in the financial markets from the other side.

The study summarized a set of conclusions, which was the most important one is the consistence of the analysis findings and the test of the main first and second hypotheses, whereas the study confirmed the mistakenness of the third hypothesis, the most important recommendation is that the companies’ management should not resort to reserve the profits excessively as a source of financing in the light of the financial crisis which would affect negatively the prices of shares of such companies in the financial markets.

Downloads

References

أ. الكتب

.1Alexander،Gordon J.,William F.Sharp,and Jeffery V. Bailey ،Fundamentals of

Investments3 ،rd ed., N.J.:Prentice-Hall, 2001.

Arlond,Glen,Corporate Financial Management,London:Financial Times Pitman

Publishing,1998.

Bodie, Zvi,Alex Kane, & Alan J. Marcus,Investments,7th ed.,Boston:McGraw-Hill, 2008.

Brealey,Rechard A.& Stewart C. Myers, Principles of Corporate Finance, 6th

ed.,Boston:Irwin/McGraw-Hill,2000.

Brooks, Chris, Introductory Econometrics for Finance, UK: Cambridge

University Press, 2002.6. Eales,Brian A.,Financial Risk Management,London:McGraw–Hill Book Company,1995.

Elton, Edwin J. and Martin J. Gruber, Modern Portfolio Theory and Investment

Analysis, 5th ed., N.Y.:John Wiley & Sons, Inc., 1995.

Jones, Charles P., Investments: Analysis and Management, 6th ed., N.Y.: John Wiley &

Sons, Inc.,1998.

Mayo, Herbert B., Investments: An Introduction, 6th ed., Fort Worth: The Dryden Press,

Pilbeam, Keith, Finance and Financial Markets, 3 rd.ed., UK: Palgrave

Macmillan, 2010.

Reilly,Frank K. and Keith C. Brown,Investment Analysis and Portfolio Management,8th

ed., Australia: Thomson,2006.

Ross, Stephen, Randolph W. Westerfield, Jefferey F. Jaffe, & Bradford D.

Jordan, Modern Finanacial Management, N.Y.: McGraw-Hill/Irwin, 2008.

Sharpe,William F. and Gordon J. Alexander,Investments,4thed.,N.J.:PrenticeHall,1990.

VanHorne,James C.,Financial Management and Policy,12th ed.,New Delhi:PrinticeHall,2004.

Weston,Fred J,Scott Besley,& Eugene F. Brigham,Essentials of Managerial Finance,11th

ed.,Fort Worth: Dryden Press,1996.

ب. البحوث المنشورة:

.16Beaver ،W., P. Kittler, M. Scholes, The Association Between Market Determined

and Accounting Determined Risk Measures ،The Accounting Review) 45 ،Oct.

(

Blume, Marchall, Betas and Their Regression Techniques, Journal of Finance, X, No.3

(June 1975).

Fama, Eugene F., Random Walk in Stock Market Prices, Financial Analysts

Journal, Vol.21, No.5, (Sebtember-October, 1965).

Klemkosky, Robert, & John Martin, The Effect of Market Risk on Portfolio

Diversification, Journal of Finance, X, No. 1 (March 1975).

Levy, Robert, On the Short-Term Stationarity of Beta Coefficients, Financial

Analysts Journal, 27, No. 5 (Dec. 1971).21. Rosenberg, Barr, & Walt McKibben, The Prediction of Systematic and Specific

Risk in Common Stocks, Journal of Financial and Quantitative Analysis, VIII, No. 2

(March 1973).

-----------------------, The Prediction of …………..: Part II, Financial Analysts

Journal, 32, No. 3 (July-Aug. 1976).

----------------------- & Vinary Marathe, The Prediction of Investment Risk:

Systematic and Residual Risk, Reprint 21, Berkeley Working Paper Series, 1979.

Sharpe, William, A Simplified Model for Portfolio Analysis, Management Science 9

(January 1963).

Thampson, Donald, Sources of Systematic Risk in Common Stocks, Journal of

Business, 40, No. 2 (April 1978).

Vasicek, Oldrich, A Note on Using Cross-Sectional Information in Bayesian

Estimation of Security Betas, Journal of finance, VIII, No. 5 (Dec. 1973).

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2012 Iraqi Journal for Administrative Sciences

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.