State space representation for synthetic time series models and BoxJackeys models with an application in the Iraqi Stock Exchange

Keywords:

boxjack models, Synthetic time seriesAbstract

The State space models is one of the ways of time series analysis which deals with the phenomena manner and its explanation through different times, these models have been used in the field of Engineering after Kalman (1960) has published his research , its using has been expanded in the other sciences such as Economics ,Medicine ,Physical Sciences ,Quality Controlling and others.

The research aims to use The State space models in the forecasting by series of numbering the daily traded shares for the Banks Sector in Iraq Stocks Exchange, it has been model every component (Trend, Seasonal and Cyclical) these components have been put in The State space model .

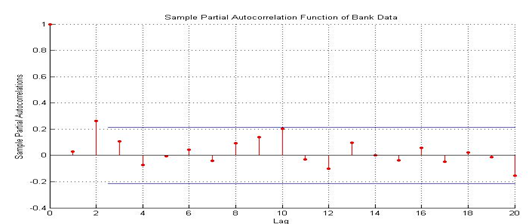

It has been built Box-Jenkins model ARMA (1, 1) for the studies series by State space model .

The Research has resulted to the Identified Model ARMA (1, 1) which has been formed by State space model is a suitable model to describe the series data during noticing results and giving it forecasting values nearer to the real while Local Level Model gave stable forecasting values and equal to (6.0112e+008), so the Researcher has recommended to depend the ARMA (1, 1).

References

الكناني . ثناء عكاب (2005) " سوق العراق للأوراق المالية (الفكرة , النشأة , النشاط) " تقرير صادر من سوق العراق للأوراق المالية .

النشرات اليومية لتداول الأسهم لعام 2006 الصادرة من سوق العراق للأوراق المالية / العلاقات العامة .

Durbin, J. and Koopman, S.J. (2001) “Time Series Analysis by State Space Methods “Oxford University Press.

Hamilton, J. D. (1994) “Time Series Analysis “Princeton University Press, New Jersey.

Harvey, A. C. (2006) “Forecasting with unobserved components Time Series Models “ Handbook of Economic Forecasting North Holland .

Janacek ,G. (2001) “ Practical Time Series “ Oxford University Press Inc. New York.

Kalman ,R. E. (1960) “ A new approach to Linear Filtering and Prediction Problems” Transaction of the ASME , Journal of Basic Engineering ,vol. 82, pp. 35-45

Kalman, R.E. and Busy, R.S. (1961) “New results in Linear Filtering and Prediction Theory “Transaction of the ASME , Journal of Basic Engineering , vol.83, pp. 95-107 .

Koopman ,S. J. , Shephard , N. and Doornik ,J.A. (1999) “ Statistical algorithms for models in state space form using SsfPack 2.2 “ Econometrics journal , volume 2 .

Makridakis ,S. Wheelwright , S. C. and Hyndman, R. J. (1998) “ Forecasting Methods and application “ 3rd edition ,John Wiley & Sons Inc. New York.

Snyder, R.D. (2004) “Exponential Smoothing: A prediction Error Decomposition Principle “.

Thanoon ,B. , Saied,B.M. and Wagih,K.S. (2006) “Application of Kalman and Extended Kalman Filtering to Target Tracking “المجلة العراقية للعلوم الأحصائية العدد 9

Wei, W.W.S. (1990) “Time Series Analysis Univariate and Multivariate Methods “Addison –Wesley Publishing Company.

Welch , G. & Bishop , G. (2004) “ An Introduction to the Kalman Filter “ , Press of university of North Carolina at Chapel Hill.

Wiener ,N.(1949) “Extrapolation ,Interpolation and Smoothing of Time Series” John Wiley &Sons , Ins. , New York.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2013 Iraqi Journal for Administrative Sciences

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

Authors retain the copyright of their papers without restrictions.